The public Chinese healthcare system is getting overcrowded. Medical resources are getting stretched thin. This is particularly evident in level III public hospitals. The government, aware of the challenges, has opened up the healthcare system to private investments as outlined in the 13th five-year plan. At the same time, Chinese government encourages physicians to practice at multiple facilities.

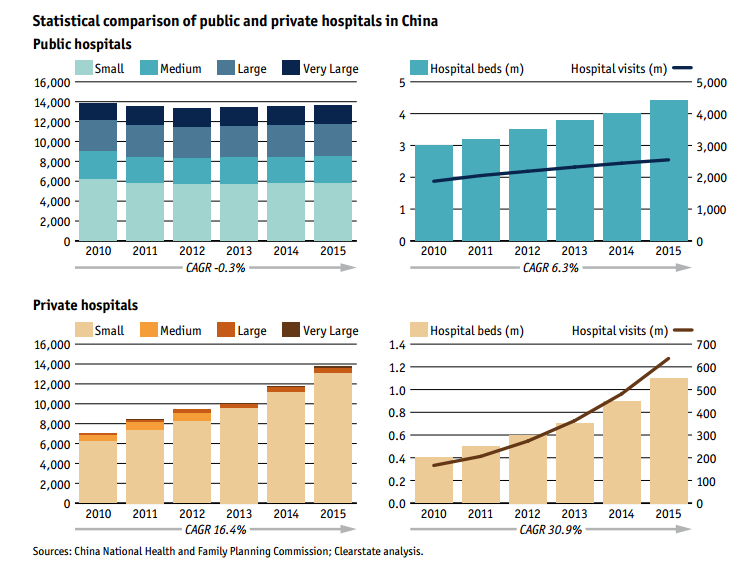

In the statistical comparison of public and private hospitals in China above from the National Health and Family Planning Commission published in 2017 the compound annual growth rate (CAGR) of public hospitals has been flat over the last 7 years while the private hospital CAGR has been 16%. The number of private hospital beds has experienced a CAGR of 31% compared to 6% for the number of beds in public institutions. Market research firm Frost & Sullivan estimated that the revenue from China’s private hospitals will triple to US$90 billion by 2019 from 2016 levels.

The rising wealth and improvement of the living standards of China’s growing middle and upper classes drive an unprecedented opportunity for private healthcare growth. Affluent local citizens favor foreign-brand medical products which usually are more readily available at the top private hospitals and level III public hospitals. In addition, Chinese government Healthcare 2020 has been trying to decentralize the concentrated care at large level III hospitals to private and lower tier hospitals. The growth of private healthcare facilities over the last seven years have experienced exponential growth.

Despite the rapid growth of private hospitals, only 10% or so services are provided by the private facilities. Level III hospitals are still very crowded especially for more serious diseases or major surgeries. For instance, on Feb 27, 2018, Beijing Cancer Hospital received 2,927 outpatients by 4 pm, well beyond its daily capacity and had to turn down any additional patient. The general private hospitals are more functioning like small community hospitals. They tend to privide more routine care.

The Chinese middle and upper classes have seen their income rise significantly as well as their expectations in medical care. In 2015 alone, Chinese citizens spent $10 billions in overseas medical care. China outbound medical tourism has grown at a rate of 500% over 3 years (It was for retaining the medical expenses that central government authorized Hainan to be the first independent province for imported medical device approval at April 4). This exponential growth is encouraging the development and construction of hospitals equipped with the latest technologies. The growth is fueling the construction of top end specialty and general private medical facilities in China. These two types of hospitals are equipped with the latest technologies, comparable to their US or European counterparts. They hire top physicians from the public level III hospitals and oversea physicians to provide the care.

Hospital groups from the UK, US and Singapore have already heavily invested in the private healthcare space in China. On Feb 2nd, 2018, representatives from International Hospitals Group, led by British Prime Minister, Theresa May, signed a contract with Keyi Real Estate for an international hospital in Hangzhou, eastern China. The total investment will be $133.7 million.

About China Med Device, LLC

China Med Device, LLC provides turn-key solutions for western medical device/IVD companies to enter China with regulation and commercialization services. Our CFDA regulatory services cover strategy, premarket submission, clinical evaluation, CRO, post market compliance as well as legal agent representation. Our commercial services cover market assessment research, reimbursement, partnership, distribution qualification and management. We have an office in Beijing, Suzhou and Boston. Our management team have 100+ years of combined experience in medical device and IVD and had been involved with 1,000+ CFDA certificates, 200+ western companies’ entry.